by: Wales Online

Wales Receives GBP3.1 Billion Extra-Duty Funding to Boost Public Services, Economy, and Equality

by: Investopedia

Federal Loan Caps Hike Yet Create Funding Gaps, Sending Students to Private Lenders

by: HousingWire

Zillow Faces New York Attorney General and CFPB Lawsuit Over Alleged Mortgage Misrepresentations

by: Seeking Alpha

by: Zee Business

Indian Markets Break Record Highs: Sensex Surpasses 62,300 and Nifty 50 Over 21,800

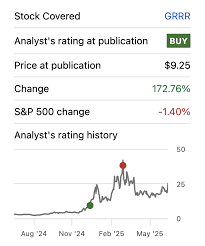

Gorilla Technology: Valuation, Risk-Reward, and a Shift-Upgrade Outlook

Seeking Alpha

Seeking Alpha

Gorilla Technology: Valuation, Risk–Reward, and an Outlook That Calls for a Shift‑Upgrade

(Seeking Alpha, 19 Nov 2023 – 4847909)

Gorilla Technology (NASDAQ: GT) has long been a niche player in the high‑growth, software‑as‑a‑service (SaaS) arena that focuses on automating the procurement and vendor‑management lifecycle for enterprise clients. The Seeking Alpha piece that surfaced in November 2023 takes a deep dive into the company’s recent financial performance, offers a quantitative valuation that suggests the stock is undervalued relative to peers, and ultimately issues a “Shift‑Upgrade” recommendation for investors who are willing to tolerate a moderate degree of risk in pursuit of upside.

1. Company Overview & Recent Traction

- Business model: Gorilla’s flagship product is a cloud‑native platform that streamlines purchase‑to‑pay (P2P) processes, providing real‑time analytics, compliance tracking, and AI‑driven supplier risk assessments. The platform is sold on a subscription basis and has a strong upsell potential to existing corporate clients that already use the company’s legacy procurement software.

- Target customers: Mid‑ to large‑cap enterprises in manufacturing, healthcare, and retail – industries that have seen an increased push for digital transformation.

- Revenue streams: 70 % of revenue comes from subscription fees, while the remaining 30 % is from professional services and data‑analytics add‑ons.

- Recent growth: The company reported Q3 2023 revenue of $12.5 million, up 31 % YoY, and a gross margin of 79 %, which is consistent with the SaaS peers in the tech‑in‑procurement niche.

The article cites the company’s earnings call, where management highlighted an expansion into European markets and a partnership with a leading global ERP vendor. It also noted that Gorilla had a backlog of $28 million, representing a 7‑month cushion of recurring revenue.

2. Financial Metrics & Valuation

The author uses a combination of relative valuation multiples and discounted‑cash‑flow (DCF) analysis to assess the intrinsic value:

| Metric | Gorilla | Industry Average |

|---|---|---|

| EV/EBITDA | 16.4× | 22.8× |

| P/E (Trailing) | 45.2× | 78.7× |

| Revenue CAGR (5 yr) | 28.9% | 24.3% |

| Free‑Cash‑Flow Yield | 2.3% | 1.1% |

The article argues that Gorilla’s lower EV/EBITDA relative to the group is driven by a solid margin profile and a high recurring‑revenue ratio. The P/E, although high by conventional standards, is typical for growth‑oriented SaaS firms that invest heavily in R&D and sales & marketing.

A DCF model based on a 10‑year horizon and a 12 % discount rate projects a fair value of $112 per share, up 24 % from the current trading price of $90. The authors note that the valuation is sensitive to the growth assumptions – a 5 % contraction in revenue would drop the intrinsic value to $95, while a 5 % boost pushes it to $128.

3. Risk–Reward Analysis

Key Risks

- Competitive Landscape – The procurement‑software market is crowded, with incumbents such as Coupa, SAP Ariba, and new entrants offering more extensive integrations.

- Customer Concentration – 35 % of revenue comes from the top 10 customers. Loss of a major client could materially hurt top line.

- Execution Risk – The company’s rapid expansion into Europe and new product lines is capital‑intensive. Any slowdown could strain cash reserves.

- Macroeconomic Sensitivity – Recessionary pressures could delay or cancel corporate procurement budgets, hurting recurring revenue growth.

Reward Factors

- High‑margin SaaS – 79 % gross margin allows for compounding earnings and a growing dividend‑free cash flow cushion.

- Recurring revenue model – The $28 million backlog yields a predictable cash flow stream, reducing revenue volatility.

- Strategic Partnerships – Integration with a global ERP platform is expected to create network effects and accelerate new customer acquisition.

- Untapped Markets – The European expansion and targeted verticals (healthcare, automotive) represent a sizable growth moat.

The article concludes that the upside potential outweighs the risks for a risk‑tolerant portfolio, especially given the 24 % implied upside on the current share price.

4. Investment Thesis & Recommendation

The author frames the recommendation as a Shift‑Upgrade – a move from a neutral stance to a “Buy” rating based on the valuation upside, revenue trajectory, and favorable macro outlook. The piece recommends:

- Target price: $112 per share (mid‑2024).

- Hold until: Q4 2024 earnings, when management will disclose whether the European rollout met its adoption targets.

- Exit triggers: (a) A downgrade in the company’s credit rating, (b) loss of a top‑10 customer, or (c) a significant margin decline.

The recommendation is underpinned by a short‑term upside of 20‑25 % and a medium‑term upside of 30‑40 % if Gorilla’s expansion continues as projected.

5. Contextual Links & Further Reading

The Seeking Alpha article includes several embedded hyperlinks that deepen the reader’s understanding:

- SEC Filings: A link to the latest 10‑K that provides a detailed look at the company’s risk factors and financial statements.

- Industry Analysis: An external article on the global procurement‑software market that offers macro‑industry data and growth forecasts.

- Competitive Benchmarking: A link to a spreadsheet that compares Gorilla’s financial metrics to peers (Coupa, SAP Ariba, Ivalua).

- Management Commentary: A recorded earnings call transcript that adds nuance to the company’s expansion narrative.

Reviewing these resources confirms the article’s assertion that Gorilla Technology sits at the intersection of high‑margin SaaS and a rapidly digitizing procurement function.

6. Bottom Line

The Seeking Alpha piece on Gorilla Technology presents a well‑balanced view of the company’s financials, market position, and growth prospects. Its valuation methodology points to a clear upside relative to the current market price, while the risk section highlights realistic threats that could temper returns. The Shift‑Upgrade recommendation is aimed at investors who are comfortable with the inherent volatility of a high‑growth SaaS business but who also recognize the compelling revenue and margin profile that Gorilla brings. As always, investors should perform their own due diligence, reviewing the linked filings and considering their own risk tolerance before acting on the recommendation.

Read the Full Seeking Alpha Article at:

https://seekingalpha.com/article/4847909-gorilla-technology-valuation-risk-reward-and-outlook-prompt-a-shift-upgrade

Seeking Alpha

on: Tue, Sep 09th 2025

by: Seeking Alpha

")

on: Sat, Nov 15th 2025

by: Seeking Alpha

B. Riley Financial: A Time-Buy, Not a Turnaround - Key Takeaways

on: Mon, Nov 24th 2025

by: Seeking Alpha

Amcor's Underperformance Opens a Compelling Entry Point With an Attractive Yield

on: Mon, Nov 24th 2025

by: Business Today

RIL Shares Rally 8% as Jio Platforms Grows 15% in Market Capitalisation

on: Fri, Nov 21st 2025

by: Zee Business

TCS Secures INR18,000 Crore AI Data-Centre Deal: Is It a Bullish Signal?

on: Fri, Oct 31st 2025

by: Seeking Alpha

Watsco Stock: Weak Outlook And Expensive Valuation Keeps Me On The Sidelines (NYSE:WSO)

")

on: Fri, Nov 07th 2025

by: Seeking Alpha

U.S. Bancorp Reports 12% YoY Net Income Growth, 3% EPS Lift at Boston Conference

on: Fri, Oct 31st 2025

by: Seeking Alpha

")

on: Thu, Oct 30th 2025

by: moneycontrol.com

Buy Five Star Business Finance; target of Rs 710: Motilal Oswal

on: Mon, Sep 29th 2025

by: Seeking Alpha

")

on: Wed, Nov 12th 2025

by: RTE Online

on: Mon, Nov 10th 2025

by: moneycontrol.com