[ Wed, Mar 11th ]: KIRO-TV

[ Wed, Mar 11th ]: Action News Jax

[ Wed, Mar 11th ]: PBS

[ Wed, Mar 11th ]: The Independent

[ Wed, Mar 11th ]: KTAL Shreveport

[ Wed, Mar 11th ]: Free Malaysia Today

[ Wed, Mar 11th ]: Sun Sentinel

[ Wed, Mar 11th ]: NOLA.com

[ Wed, Mar 11th ]: People

[ Wed, Mar 11th ]: Post and Courier

[ Wed, Mar 11th ]: WWTI Watertown

[ Wed, Mar 11th ]: WPIX New York City, NY

[ Wed, Mar 11th ]: The Baltimore Sun

[ Wed, Mar 11th ]: PC World

[ Wed, Mar 11th ]: Town & Country

[ Wed, Mar 11th ]: Seeking Alpha

[ Wed, Mar 11th ]: Tennessean

[ Wed, Mar 11th ]: Forbes

[ Wed, Mar 11th ]: Bravo

[ Wed, Mar 11th ]: Telegram

[ Wed, Mar 11th ]: Business Insider

[ Wed, Mar 11th ]: Investopedia

[ Wed, Mar 11th ]: CNN

[ Wed, Mar 11th ]: Maryland Matters

[ Wed, Mar 11th ]: COMINGSOON.net

[ Wed, Mar 11th ]: Patch

[ Wed, Mar 11th ]: CNBC

[ Wed, Mar 11th ]: WFXT

[ Wed, Mar 11th ]: WHIO

[ Wed, Mar 11th ]: Fortune

[ Wed, Mar 11th ]: reuters.com

[ Wed, Mar 11th ]: Buckeyes Wire

[ Wed, Mar 11th ]: The Financial Times

[ Wed, Mar 11th ]: Heavy.com

[ Tue, Mar 10th ]: Detroit News

[ Tue, Mar 10th ]: Investopedia

[ Tue, Mar 10th ]: The Center Square

[ Tue, Mar 10th ]: BBC

[ Tue, Mar 10th ]: deseret

[ Tue, Mar 10th ]: Seeking Alpha

[ Tue, Mar 10th ]: Daily Express

[ Tue, Mar 10th ]: Euronews

[ Tue, Mar 10th ]: ThePrint

[ Tue, Mar 10th ]: MassLive

[ Tue, Mar 10th ]: The Financial Times

[ Tue, Mar 10th ]: Reuters

[ Tue, Mar 10th ]: Fortune

[ Tue, Mar 10th ]: CNN

SAVE Plan Borrowers Face Unexpected Ineligibility

Investopedia

InvestopediaLocale: UNITED STATES

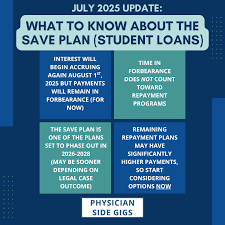

Washington D.C. - March 11, 2026 - Millions of student loan borrowers enrolled in the Biden administration's Saving on a Valuable Education (SAVE) plan are facing a critical juncture as the Department of Education continues implementing long-delayed income-driven repayment (IDR) account adjustments. While initially hailed as a lifeline for debt-burdened Americans, the adjustments are unexpectedly forcing a significant number of borrowers to re-evaluate their repayment options, potentially leaving the SAVE plan altogether.

The SAVE plan, rolled out in 2024, promised reduced monthly payments and a pathway to loan forgiveness after 20 years for eligible borrowers. It represented a cornerstone of President Biden's broader student loan forgiveness efforts, aiming to alleviate the financial strain of higher education debt. However, the ongoing IDR account adjustments - designed to correct historical errors in loan tracking and credit toward forgiveness - are having a ripple effect, pushing many borrowers over the income thresholds required to remain on the SAVE plan.

These adjustments aren't simply administrative tweaks; they are recalculations of a borrower's loan history, accounting for periods of forbearance, deferment, and different repayment plan enrollments. The goal is to accurately reflect the total qualifying months toward loan forgiveness under IDR plans. But the very process of correcting past inaccuracies is triggering income recertification requirements for many, often revealing incomes higher than previously reported or assumed.

"The adjustments that borrowers are seeing are a positive development in the sense that they are fixing errors and ensuring correct loan accounting," explains Travis Horn, founder of The Student Loan Compass, a leading resource for student loan borrowers. "However, the unfortunate byproduct is that many borrowers are now finding themselves ineligible for the SAVE plan based on their updated income."

The issue isn't necessarily that borrowers' incomes have increased dramatically. Rather, the adjustments are shining a light on existing income levels that were previously underreported or not properly accounted for within the IDR system. This could be due to various factors: borrowers taking on second jobs, receiving bonuses, or experiencing wage growth over the past few years. The Department of Education relies on self-reported income data, and the adjustments are effectively triggering a more rigorous verification process.

Beyond SAVE: What Options Do Borrowers Have?

For borrowers deemed ineligible for SAVE, several alternatives exist. These include other income-driven repayment plans like Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Income-Contingent Repayment (ICR). Each plan has its own eligibility criteria and repayment terms, making careful consideration crucial. Some borrowers may even find that a standard fixed-rate repayment plan, potentially through refinancing with a private lender, offers a more favorable long-term solution.

However, navigating these options can be daunting. The complexity of the federal student loan system is a well-documented problem, and the IDR adjustments have added another layer of confusion. Many borrowers are unaware of their options or struggle to understand the implications of each plan.

The Urgency of Recertification and the Risk of Default

The Department of Education is urging borrowers to proactively update their income information. Failure to do so could lead to inaccurate loan balances and, ultimately, default. The grace period for recertification is typically limited, adding to the pressure on borrowers.

Experts are advising borrowers to begin the recertification process immediately. This involves submitting updated income documentation to the Department of Education through the Federal Student Aid website. It's also advisable to review loan statements carefully and contact the loan servicer with any questions or concerns.

Looking Ahead: Systemic Issues and Potential Reforms

The current situation highlights the deep-seated issues within the federal student loan system. The need for greater transparency, simplified repayment options, and more effective communication with borrowers is becoming increasingly apparent. The Biden administration has signaled its commitment to addressing these challenges, but significant reforms will likely require congressional action.

The long-term impact of the IDR adjustments and the exodus from the SAVE plan remain to be seen. However, it's clear that millions of borrowers are facing a period of uncertainty and require access to clear, accurate information and effective support to navigate this evolving landscape. The Department of Education faces a significant challenge in ensuring a smooth transition and preventing widespread defaults. The future of student loan repayment is being reshaped, and borrowers must be proactive to protect their financial well-being.

Read the Full Investopedia Article at:

[ https://www.investopedia.com/millions-of-borrowers-will-need-to-leave-biden-era-student-loan-repayment-plan-11922949 ]

[ Mon, Feb 23rd ]: Investopedia

[ Mon, Feb 23rd ]: Investopedia

[ Sun, Feb 22nd ]: Investopedia

[ Sun, Feb 15th ]: 13abc

[ Sat, Jan 31st ]: Business Insider

[ Fri, Jan 23rd ]: Investopedia

[ Tue, Jan 20th ]: The Messenger

[ Thu, Jan 08th ]: Investopedia

[ Wed, Jan 07th ]: Investopedia

[ Mon, Jan 05th ]: Investopedia

[ Sun, Jan 04th ]: Investopedia

[ Tue, Dec 09th 2025 ]: Investopedia