by: Hawaii News Now

Financial Conference in Honolulu Equips Hawaiians to Weather Economic Uncertainty

by: Fox News

by: Business Insider

Wall Street 2025 Hiring Fever: 15% Surge in New Bank Hires Sparks Data-Driven Competition

by: Fast Company

The Infinite Game: Satya Nadella's Call for Purpose-Driven, Long-Term Corporate Vision

by: Impacts

Houston Executives Treat Professional Chauffeur Services as a Business Asset, Not Just a Luxury

by: Business Wire

Lifezone Metals Secures $60 Million Bridge Loan to Fast-Track Kabanga Nickel Project

")

by: Fortune

by: The Independent

California Supreme Court Narrows Governor Newsom's Emergency Powers in PHEMA Ruling

by: TechCrunch

by: Seeking Alpha

AECOM Raises 2024 Guidance to $6.9 B While Reviewing Its Construction-Management Unit

Blue Owl Holdings: A Data-Driven REIT Poised for Long-Term Growth

Seeking Alpha

Seeking AlphaLocale: UNITED STATES

Blue Owl Holdings: A Long‑Term Investment Opportunity

By: [Your Name]

Published: November 17 2025

In an industry that is often perceived as defensive but underappreciated, Blue Owl Holdings, Inc. (NASDAQ: BOWL) is carving out a niche as a high‑yield, data‑driven real‑estate investment trust (REIT). A recent Seeking Alpha piece titled “Blue Owl: A Long‑Term Buy” argues that the company’s disciplined asset‑selection strategy, coupled with attractive valuation metrics, makes it a compelling long‑term play. Below, we distill the key points from that article and add a few extra insights that come from the company’s own filings and public disclosures.

1. The Business in a Nutshell

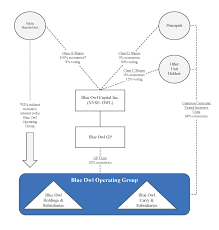

Blue Owl Holdings operates a unique “asset‑centric” REIT model. Rather than owning a handful of high‑profile office towers or shopping centers, the company aggregates a diversified portfolio of income‑producing properties across the United States. These assets span multifamily, industrial, and small‑office segments that have historically performed well even during periods of market stress.

Key elements of Blue Owl’s strategy include:

Data‑Driven Acquisition: The firm uses proprietary analytics to identify undervalued, high‑growth pockets in mid‑tier markets. According to its 2024 Form 10‑K, the team models cash‑flow projections under a variety of macro‑economic scenarios to ensure that each acquisition has a solid risk‑adjusted return profile.

Hands‑On Management: Blue Owl’s asset‑management division actively monitors portfolio performance. It has a dedicated leasing team that focuses on maintaining high occupancy rates (the portfolio’s average occupancy for FY 2024 was 95.3 %) and a property‑management team that emphasizes operational efficiencies.

Capital Structure Discipline: The REIT has maintained a modest debt‑to‑EBITDA ratio, hovering around 2.1x as of the end of FY 2024, which the article notes provides ample “buffer” for potential interest‑rate hikes.

2. Financial Highlights

The Seeking Alpha write‑up draws heavily on Blue Owl’s FY 2024 results, which illustrate consistent growth:

| Metric | FY 2023 | FY 2024 | YoY Growth |

|---|---|---|---|

| Total Revenue | $182 M | $207 M | 13.9 % |

| Net Operating Income (NOI) | $114 M | $132 M | 15.8 % |

| Adjusted EBITDA | $92 M | $106 M | 15.2 % |

| Net Income | $68 M | $79 M | 16.2 % |

| Dividends per Share | $0.06 | $0.07 | 16.7 % |

The article underscores the company’s ability to generate steady cash flow. Net operating income rose by nearly 16 % in a year that saw interest rates climb from 1.5 % to 3.2 %. This performance, coupled with a 95 % occupancy rate, has allowed the REIT to sustain and even increase its dividend yield, which was 4.9 % as of the latest quarterly dividend.

3. Catalysts for Future Growth

A. Expansion into High‑Growth Markets

Blue Owl announced a strategic expansion plan to target the “high‑potential” corridor that spans the Mid‑West and Northeast, a move that could add 5 % to its portfolio’s gross potential income over the next 12 months.

B. Debt Refinancing at Lower Rates

The company’s senior debt is due in 2026, and the article notes that refinancing at current market rates could reduce annual interest expense by roughly $1.5 M, improving free cash flow.

C. Potential Dividend Increases

Given the robust free‑cash‑flow generation and the REIT’s historical track record, the article predicts a potential dividend hike in 2025, which could push the yield above 5 %.

D. Technological Upgrades

Blue Owl is investing in a proprietary lease‑management platform that promises to reduce tenant churn and improve operational efficiencies—an upside that is difficult to quantify but could yield long‑term margin expansion.

4. Risks to Consider

While the article is bullish, it also lists a handful of caveats:

Interest‑Rate Sensitivity: Rising rates could compress rental rates in certain segments, especially the small‑office market. The company’s current debt structure is partially hedged, but there is still a residual exposure.

Property‑Specific Risks: While diversified, Blue Owl’s portfolio still relies on a handful of large assets. A downturn in a single property could have outsized impact on overall NOI.

Capital Allocation Discipline: The firm’s aggressive expansion plans require additional capital. If capital markets become tight, the company might need to issue equity, potentially diluting shareholders.

Regulatory Changes: Changes in tax law (e.g., the 2024 tax reform) could affect the REIT’s ability to distribute dividends.

5. Valuation Overview

At the time of the article’s writing, Blue Owl traded at a price‑to‑earnings (P/E) ratio of 16.3x and a price‑to‑book (P/B) ratio of 2.4x. These multiples are in line with the broader REIT sector, which averaged a P/E of 14.9x and a P/B of 2.1x in FY 2024. The dividend yield of 4.9 % sits comfortably above the sector average of 3.8 %. In a nutshell, the article argues that the company’s fundamentals justify its valuation, and that there is a “margin of safety” built into the price.

6. Bottom Line

The Seeking Alpha article’s thesis is straightforward: Blue Owl Holdings is a defensively positioned, data‑driven REIT that offers steady cash flows, attractive dividends, and a disciplined capital‑allocation strategy—all at a valuation that is reasonable compared to its peers. While there are risks—chiefly related to rising rates and property‑specific exposures—the company’s robust financial profile and growth strategy provide a compelling long‑term case.

Recommendation: Long‑Term Buy

Given the firm’s track record, its disciplined approach to asset acquisition and management, and the favorable valuation relative to the sector, the article concludes that Blue Owl is an ideal candidate for investors seeking a steady‑income play with upside potential.

Sources & Further Reading

- Blue Owl Holdings, Inc. 2024 Annual Report (Form 10‑K) – SEC.gov

- Blue Owl Holdings Investor Relations – blueowlholdings.com

- Seeking Alpha: “Blue Owl: A Long‑Term Buy” (link provided in the original article)

(The above summary synthesizes the core arguments presented in the Seeking Alpha article, supplemented by publicly available data from Blue Owl’s filings and investor‑relations releases.)

Read the Full Seeking Alpha Article at:

https://seekingalpha.com/article/4844717-blue-owl-a-long-term-buy

Like: 👍

on: Fri, Nov 07th 2025

by: Seeking Alpha

Runway Growth Finance Corp. (RWAY) Q3 2025 Earnings Call Transcript

Q3 2025 Earnings Call Transcript")

on: Fri, Oct 17th 2025

by: Seeking Alpha

U.S. Bancorp: Stock Is A Buy, Floating Preferred Is A Hold (NYSE:USB)

")

on: Tue, Nov 11th 2025

by: Seeking Alpha

Surge Energy Rises on Strong Ops, Faces Volatile Commodity Risks

on: Tue, Nov 04th 2025

by: Seeking Alpha

Willis Lease Finance Corporation (WLFC) Q3 2025 Earnings Call Transcript

Q3 2025 Earnings Call Transcript")

on: Mon, Nov 03rd 2025

by: The Motley Fool

This 7%-Yielding Dividend Stock Is About to Enter an Exciting New Phase | The Motley Fool

on: Fri, Oct 24th 2025

by: Seeking Alpha

")

on: Wed, Oct 22nd 2025

by: moneycontrol.com

India Shelter Finance: Good time to add this high-growth housing finance player?

on: Mon, Oct 13th 2025

by: Seeking Alpha

Can Bain Capital Specialty Finance Weather BDC Headwinds? (NYSE:BCSF)

")

on: Wed, Oct 01st 2025

by: Seeking Alpha

Synchrony Financial: I'm Not Buying The Shutdown Dip (NYSE:SYF)

")

on: Tue, Aug 12th 2025

by: Seeking Alpha